Starbucks Corp. (SBUX) plans to debut its stores in India by mid-2007 through a joint venture with an Indian partner, RPG Enterprises. Though the negotiations are still going on, unconfirmed reports say that Starbucks will have a 51% stake in the joint venture while RPG will have the remaining 49% stake. RPG will also be the new venture's master franchisee. RPG is one of India's largest conglomerates with significant interests in power, retail, entertainment and technology among others. RPG has beaten other large Indian groups like Reliance Industries and Bharti Enterprises to convince Starbucks. With retail operations in major cities in India, RPG will be able to provide Starbucks with local cultural, economic, operating and franchising expertise, and may also lend its retail network.

New Delhi and Mumbai, the national and financial capitals will see the first stores by mid-2007. Starbucks will also be looking to add 100 stores every year for the next five years. Even though this strategy looks aggressive, it makes sense. Though India is traditionally a tea drinking nation there is a lot of coffee consumption and other malt-based drinks. Coffee culture in India has been getting bigger in India. Reports indicate that customers at existing retail coffee shops are students and professionals between 18 and 35 years old. Big coffee retail players in India like Barista (with Tata and an Italian partner), Costa Coffee (based in UK), Cafe Coffee Day (funded by Sequoia) and Barnie's (based in US) have aggressive expansion plans and are adding new drinks apart from Coffee. These players are also using a variety of different approaches to attract new mass and premium clientele. So Starbucks faces very fierce competitors in India.

This is where RPG's assets and expertise will be helpful to Starbuck's India strategy. With RPG's strength in entertainment and other upscale retail space, it can hope to direct some consumers to the new Stabucks' stores. They will also have to customize its drinks for the Indian market. Pricing will also be a factor to consider as Starbucks cannot translate its US prices in India. Starbucks experience with its Chinese operations will offer some ideas in this regard. With a burgeoning middle-class in India, Starbucks needs to attract only a small percentage of them along with students and professionals with high disposable incomes to easily entrench itself in the Indian market.

Though Starbucks does not have a first mover advantage, it is entering an already tried, tested and proven market along with a local player with strong retail expertise giving Starbucks an advantage along with its strong brand. This move will provide strong long-term growth opportunities for Starbucks.

(This article was published as "Starbucks' India Strategy Looks Promising" on SeekingAlpha on October 2, 2006.)

Labels: India, SBUX

American Technology Research Analyst, Shaw Wu has commented that Zune, the new media player from Microsoft (MSFT) will hurt Microsoft and it's partners more than it will hurt Apple (AAPL) or it's iPod. Though the price tag for Zune, $249.99 is similar to a comparable iPod's price, Wu thinks that it will be difficult to convert iPod users to Zune. Wu also estimates that Microsoft will lose $50 for every Zune it sells. Wu's sources indicate that Microsoft did not expect Apple to lower prices of its iPods. This move had surprised Microsoft and had forced it to reduce pricing to match Apple's. Wu also commented on the superior supply chain and operating efficiency of Apple which is highly invisible. This probably has given Apple the edge over the new Zune threat by allowing Apple to lower the iPod prices. In this price range, Apple still makes profits while Microsoft loses money.

While many people cite Microsoft's success with Xbox, it is a completely different game than media players. Media players have small form factors and a lot of content to navigate. I repeat NAVIGATE. This is the key to iPod's success. The click wheel makes combing through a vast library of media easy. Whereas in Zune, one has to scroll through the library individually, making it difficult to move around. Zune's user interface, based on Windows will not provide a good experience. In the initial comparisons, Zune seems to have a lesser battery life than iPod, which is again a let down. The wireless or WiFi feature that allows networking and sharing is a novel concept. But you should enough Zune users around you to share with. Connecting to a wireless network and allowing other people to communicate with your device is a cumbersome process, a drain on the battery and not to mention issues associated with hacking or viruses. While you are waiting at a traffic signal or traveling in a train, you dont want anyone to hack into your player and erase all your music. Security is a key feature that not many people are talking about and we probably will wait for more information to be revealed. Zune has a bigger screen than the iPod. Well is this really an advantage or a disadvantage? If you want to watch videos it is good but if you just want to listen to music, then you probably will not need this big a screen. So the overall user experience of Zune may not stand up to iPod's user experience. There is also the question of how Zune's Marketplace with stack up with the iTunes Store. There is one area where Microsoft has the edge, gaming. If Microsoft is capable of somehow incorporating games into Zune and allowing a network of users to play games, it has a chance to get into a territory that Apple is weak in. This is understandable with Zune's screen size and wireless capability. But the current design of Zune is not game-friendly.

There are many products which have been successful in the past because of their user experience even though they had lesser features than their competitors. Zune with more features is simply not enough to challenge the iPod. It needs to be seen how long Microsoft can lose money, churn out new 'Zunes' and market its features and brand to gain an edge over Apple.

Wu also estimates that, Apple has 18-22% gross margin and 8-11% operating margin. So Microsoft will not only have to overcome Apple's prolific innovations and designs but has to atleast match Apple's operating efficiency to kill the iPod.

On a sidenote, another effect of Microsoft's foray into the media player business is antagonizing some of its partners. Since Microsoft has the upper hand on its partners now, it is not an issue. But Microsoft may feel the heat later on when it may need their help.

Labels: AAPL, MSFT, Tech, UX

Yesterday, Walt Disney Co. (DIS) CEO Robert Iger told a Goldman Sachs (GS) investor conference, Communacopia that the company has sold 125,000 movies through Apple (AAPL) iTunes store, generating a revenue of $1 million. Considering that with just 75 movies and in a single week, this is a smashing result. Iger also expects iTunes movie downloads to generate revenues of $50 million in the first year. This is a significant number and is worth noting as other Hollywood studios may find this kind of revenue hard to resist. Iger also expects to increase the number of digital content offerings as licensing issues are sorted out.

Amazon (AMZN) has not revealed how its service, Unbox has fared. Compared with Unbox, Movielink and other services, Apple may have the best digital distribution network of all. So we can expect relations between movie studios and Apple to warm up and start discussions. It is not clear how revenue is shared between Apple and Disney now. But from past behavior, Apple may not lose too much money on bandwidth costs, which is a major cost in digital distribution.

All this is happening without Apples's iTV or any clear solution to transfer content from a computer to TV. If iTV provides a simple and effective solution to this problem and convince consumers to use it, then Apple will get more leverage over other movie studios.

Iger made another comment about overhauling Disney.com and relaunching it. Although he did not elaborate on this idea, Disney may be creating various channels of entertainment, in the style of YouTube in a move to use Disney.com to deliver digital content or redirect visitors to iTunes.

Labels: AAPL, AMZN, DIS, GS

Google (GOOG) is down $17.49 or 4.22% to $397.20, Yahoo (YHOO) is down $3.60 or 12.41% to $25.40, Amazon (AMZN) is down $0.87 or 2.71% to $31.21, eBay (EBAY) is down $1.18 or 4.4% to $25.66, CNET (CNET) is down $0.74 or 7.66% to $8.92 and IAC Interactive (IACI) is down $0.53 or 1.86% to $27.89.

Yahoo's CFO, Susan Decker has warned of lower sales for Q3, because of weakness in the Auto and Financial sector ads. IACI Chairman, Barry Diller had mentioned that IACI is seeing weakness in Financial sector. This may not be isolated to these two companies but a reflection of the entire sector. Although both the executives did not quantify how bad the slowdown is, expectations are worse and there is a big sell-off. This is probably a knee-jerk reaction and I expect the stocks to move up cautiously this week.

Labels: AMZN, CNET, EBAY, GOOG, IACI, YHOO

Walmart (WMT) may have inadvertently revealed the price of Microsoft (MSFT) Zune player. According to Walmart.com, Zune is priced at $284. Gadget blog, Engadget has pictures of a cached Google page, showing Zune's price. Walmart.com has removed the pricing from the main page. Unless Walmart.com pulls down those details, you can still follow this link to see a comparison of a 30 GB iPod and the Zune player which will show the price. The title of the Zune player says "Zune 30 GB MP3 / Video Player", although features of Zune are not listed for comparison. As far as digital formats are concerned, Walmart.com says that Zune will be capable of automatically importing 'most' music from iTunes and Windows Media Player. If you bring your own content, it has to be in the following formats - Music: WMA, MP3, AAC; Photos: JPEG; Videos: WMV, MPEG-4, H.264.

Labels: MSFT, WMT

Nabors Industries Ltd. (NBR), registered in Bermuda and headquartered in Barbados is the largest land and platform oil, gas and geothermal drilling contractor in the world, with a 20-24% market share. As of March 2006, Nabors operates in US, Canada, Middle East, Australia, South America and Africa by owning or operating a fleet of 3 barge rigs, 19 jack-ups, 28 marine vessels, 43 platforms, 588 land drilling rigs and 781 land workover rigs. Nabors is the largest rig owner and operator in the US. Nabors has operations in a lot of international markets and is very diversified geographically, thereby diluting the impact of geopolitical events.

A large portion, a little more than 90% of Nabors revenue comes from contract drilling services, while the remainder comes from other services like oil field management, engineering, transportation and logistics services.

For the past five years, Nabors shares have appreciated 150% while Exxon Mobil (XOM) shares have appreciated 50%. Since NBR listed in February 1991, NBR has appreciated 650% while XOM appreciated 400%. Nabors is included in the S&P 500. In August, Nabors announced plans to repurchase $500 Million worth of common shares. Nabors shares, on September 15, closed at 30.06, near a 52-week low, providing a good buying opportunity. With a TTM P/E of 11 and a forward P/E of 7, Nabors shares are very attractive. Taking TTM values and comparing it to its peers, Nabors P/E is lower, P/S is lower, EPS is higher, sales growth is higher and ROI is lower. In 2004, revenue was $2.39 Billion and in 2005 revenue was $3.55 Billion. Analysts average estimates of revenue for 2006 and 2007 are $4.88 Billion and $5.95 Billion respectively. Nabors balance sheet shows strong cash flow, revenue and growth, indicating financial strength. Nabors has a strong management capable of taking the company through ups and downs.

In the first quarter of 2006, day rates for American land drilling rose by $1,475 per day to $18,695 and cash margins rose by almost $1,000 a day to about $9,600. This was a record high. In the second quarter of 2006, day rates rose by $1,491 per day to $20,186 and cash margins rose by $1,257 per day to $10,858. This was again a record high. Most of the existing contracts were negotiated in the year 2005. Some of the contracts expire before the end of 2006. And in 2007 many more are expiring. When the contracts are renegotiated, there is a high probability that Nabors can demand longer contracts and higher day rates which can boost its revenues without a significant increase in costs and also decrease earnings volatility. Over the long term, demand for contract drilling is expected to increase in the US as well as in international regions. With rig supply limited, day rates for drilling are expected to increase, especially in international regions where Nabors will have more pricing power.

Demand for oil and gas is increasing all over the world. Drilling so far has mainly been to create relatively shallow wells. In the case of natural gas, reserves below 15,000 feet of the earth’s surface largely remain untapped. Future exploration will concentrate on drilling wells below 15,000 feet. To maintain the current natural gas production of 18.5 Tcf (Trillion Cubic Feet), more than 15,000 wells must be drilled, which is a conservative estimate. Just in the US, proven conventional gas resources are estimated at 192 Tcf. Of these resources, only 1% of them are deep wells. As of June 2006, US Department of Energy (DoE) estimates that, US onshore and offshore deep reservoirs hold 169-187 Tcf of gas resources. DoE also estimates that for ultra-deep wells, drilling the last 10% of the well alone will cost 50% of total cost of the creating the well. As deeper and more complex wells are drilled, total expenditure on rigs will also increase. All this creates an advantage for Nabors.

Oil and gas exploration is not going to slow down any time soon, especially natural gas. Companies are trying to figure out future energy supplies and are spending a lot of capital towards these goals. As reserves are getting below normal levels, drillers have to drill deeper holes. Nabors, offering contract drilling services, can easily capitalize on this demand. It is not very easy to change drilling contractors and if Nabors has enough pricing power, which it has, Nabors can command higher rates.

Oil and gas prices have come down from their recent peaks. But they still are high. If the prices keep going down, it will pull down the entire oil and gas sector down, resulting in reduction in contract drilling day rates. But if they remain high for the next couple of years, Nabors tends to benefit from it, providing a strong upside.

The bottomline is that exposure to international markets, new contracts and a bullish natural gas sector provide a huge growth opportunity for Nabors. If this trend continues, Nabors stock will not stay in this price range for long. Whereas, high drilling costs may lead producers to reduce capital expenditures on new drilling hurting Nabors’ growth rate which may cause the stock to remain stagnant.

(This article was published as "Nabors Should Capitalize On Strong Natural Gas Demand" in SeekingAlpha on September 19, 2006 and as "Drilling Deeper into Nabors (NBR)" in GuruFocus on September 20, 2006.)

Labels: NBR, XOM

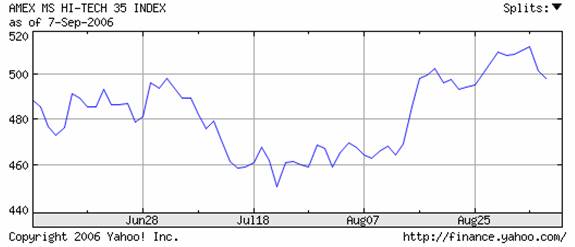

In the past one month, the oil sector has slowly eased while the technology sector has gained traction.

When you compare the two indices for August and September, the Morgan Stanley High Technology Index (MSH) and the AMEX Oil Index (XOI), one can clearly see that Oil's loss was Technology's gain.

This may be the sign of things to come in the next few months. Stock market statistics show that the performance of the oil stocks are tied to the price of oil. As the price of oil begins to fall, oil stocks are getting more risky.

The positive news about the technology bellweathers has propelled the technology stocks in recent weeks. In the next 3-6 months, technology stocks can be expected to deliver a strong performance.

Labels: Sector

Pharmaceutical stocks are getting a lot of traction in recent weeks and Dr. Reddy's Laboratories Limited (RDY) seems to have joined the race. Reddy's (RDY) turnaround has been remarkable. In the past 12 weeks, Reddy's has beaten S&P 500 by about 10%.

Merck & Co, Inc (MRK) has recently authorized Reddy's to produce versions on Proscar and Zocar. FDA has also approved Merck's (MRK) Propecia to be manufactured by Reddy's. Along with Allegra, Reddy's has four major generics coming out soon with very good sales potential. With more generics in its pipeline waiting for FDA approval, Reddy's is strongly set for growth.

Reddy's is a fairly geographically diverse company with operations in developed economies like US and Germany and well as in developing economies like India and Mexico. Reddy's recent acquisitions in Germany (Betapharm) and Mexico (Roche's API) will also increase Reddy's revenue growth and profitability. Trading at below $32 now, with a forward P/E of 20.82, Reddy's stock can easily move above $37 in the next 6 months.

(This article was published as "Reddy's is Ready for Aggressive Growth" in SeekingAlpha on September 05, 2006.)

Labels: MRK, RDY

Intel (INTC) is widely expected to announce on September 5, 2006 (Tuesday) that it will be laying off about 10,000 workers, almost 10% of its workforce. The results of a three-month analysis of its entire operations with the aim of cutting $1 billion in costs are expected by the end of Q3. If this reduction in workforce happens, the total reduction in recent months will be 13,000, that comes close to Wall Street expectations of 16,000. This might just be the right news to kickstart growth in the INTC stock price, which closed at $19.57 yesterday.

Are the dog days for INTC over? If you are looking at semiconductor/chip stocks, I think this is the right opportunity to get in to INTC.

For starters, with this recent news, Wall Street analysts will not be as skeptical as they were. Intel's high inventory levels are starting to decline as it competes with Advanced Micro Devices (AMD) by reducing prices. Intel has a new lineup of 64-bit processors to be coming into the market soon. Independent chip reviewers have conceded that new Intel chips handsomely beat rival AMD chips in many benchmarks. With the memory intensive Microsoft (MSFT) Windows Vista being expected within the next four months, INTC can expect an increase in demand for its new products. The recent positive indicators in its WiMAX strategy to provide affordable wireless broadband access are also worth noting.

With a long corporate history, lower debt compared to its competitors, a strong brand name recognized all over the world, new superior products, a lean-and-mean INTC stock is all set to be loved by Wall Street. I will be waiting and watching how high the stock will fly in the next 3-6 months.

(This article was written on September 01, 2006 and I am still bullish on Intel.)

Labels: AMD, INTC, MSFT